Tax rebate loans are short-term financing secured against your expected ATO refund. For eligible startups, the underlying R&D Tax Incentive can be valuable because companies under $20 million aggregated turnover may access a 43.5% refundable offset on eligible R&D expenditure, but borrowing against that future refund is often an expensive way to solve a timing problem.

You're probably here because the timing hurts. You've paid engineers, cloud bills, contractors, and product costs. Your R&D claim may be legitimate, material, and well underway. But payroll lands this month, not when the refund eventually arrives. That gap is where lenders, tax-time loan providers, and some advisers step in.

My view is simple. Most founders should treat tax rebate loans as a last resort, not a default funding tool. They can look tidy on a spreadsheet because they're tied to an expected refund, but the refund is still an estimate until the claim is properly prepared, lodged, and processed. If the estimate moves, your loan risk doesn't disappear. It just becomes your problem faster.

A better approach is to tighten documentation, get the claim prepared earlier, and reduce avoidable lag in the process before taking on debt. That preserves equity better than raising a panic bridge, and it usually protects runway better than borrowing against an asset you haven't received yet.

If you want background on the team behind this publication, see ClaimKit's company overview.

Table of Contents

- Introduction

- What Exactly Are R&D Tax Rebate Loans?

- How Do These Loans Work and What Are the Risks?

- Are There Better Alternatives to Tax Rebate Loans?

- Can You Avoid a Loan by Accelerating Your R&D Claim?

- A Founder's Checklist for Choosing a Funding Path

- Frequently Asked Questions About R&D Funding

Introduction

A founder closes the month, looks at the bank balance, and realises the expected R&D refund won't solve next week's payroll problem. That's the exact moment tax rebate loans become tempting. The pitch is straightforward. Borrow now, repay later from the ATO refund.

That simplicity is why these products get traction. The problem is that they compress a compliance process into a credit product. If your claim is late, weakly documented, or overestimated, the lender still expects repayment under the loan terms.

Practical rule: If cash is tight because your claim prep started late, fix the process first. Debt should solve a genuine short-term timing issue, not cover poor documentation or a rushed EOFY workflow.

For Australian tech startups, the context matters. The R&D Tax Incentive on business.gov.au exists to support eligible companies doing genuine innovation work, including software and engineering projects. It isn't designed to be a financing product. Founders turn it into one when they borrow against it.

That's why I'm cautious. The incentive can be a strong source of non-dilutive support for eligible companies. But a tax rebate loan inserts cost, lender conditions, and often adviser conflicts into a process that already needs care. If you're pre-seed to Series A, preserving flexibility matters more than chasing convenience.

This comes up most often around EOFY, after a fundraising delay, or during a hiring ramp where expenses have landed before revenue has caught up. In those situations, you need a decision framework, not optimism. Work out whether the claim is solid, whether timing can be improved, and whether debt is genuinely cheaper than the alternatives.

What Exactly Are R&D Tax Rebate Loans?

An R&D tax rebate loan is a short-term loan secured against an expected refund from Australia's R&D Tax Incentive. It's a specialised version of a broader product category often called a refund anticipation loan. The distinction matters because an R&D claim is more technical, more document-heavy, and more exposed to eligibility questions than a standard personal tax refund.

Why lenders care about R&D refunds

Lenders care because the underlying program is large and widely used. In the 2023-24 income year, Australia's R&D Tax Incentive hit a record with 13,901 companies registering and reporting $17.7 billion in estimated R&D expenditure, while $4.0 billion in refundable offsets went to 10,882 companies, according to Prime Partners' R&D Tax Incentive statistics summary.

That scale tells you two things. First, founders are right to pay attention to the incentive. Second, any pool of expected refunds that large will attract loan products, brokers, and advisers.

For startups under $20 million aggregated turnover, the incentive is especially meaningful because eligible companies may receive a 43.5% refundable offset on eligible R&D expenditure, while companies above that threshold receive a 38.5% non-refundable offset, as outlined in the OECD INNOTAX entry for Australia. The same OECD entry notes that up to AUD 150 million of R&D expenditure per income year is eligible for those offset rates, and that the current minimum expenditure threshold is AUD 20,000.

What founders are really borrowing against

You're not borrowing against cash in the bank. You're borrowing against an expected future outcome from a claim that still needs to stand up on eligibility, documentation, and lodgement quality.

Eligible R&D activities must aim to generate new knowledge, follow a systematic progression involving hypothesis and experimentation, and involve outcomes that aren't predictable in advance, as explained in this startup-focused R&D eligibility guide. For software teams, that usually means the difference between claiming real technical uncertainty and trying to relabel ordinary product work as R&D.

This can be understood in a straightforward manner:

| Product | What it's secured against | Main issue |

|---|---|---|

| Refund anticipation loan | A general expected tax refund | Often treated as routine short-term credit |

| R&D tax rebate loan | An expected R&D Tax Incentive refund | Depends heavily on claim quality and evidence |

If you want a broader perspective on how debt can interact with tax planning, this guide on smart tax planning with loans is worth reading. Use it as context, not as a reason to assume an R&D-linked loan is automatically sensible for a startup.

The more uncertainty in the claim, the less attractive the loan should be.

How Do These Loans Work and What Are the Risks?

The usual process sounds harmless. A lender or intermediary asks for your expected refund amount, some company financials, and details of the claim. They assess the likely receivable, issue a loan offer, advance cash, and expect repayment once the refund arrives.

That's the clean version. Real life is messier.

The loan is priced off an estimate, not a certainty

Your expected refund may change. Costs can be reclassified. Activities can be challenged. Supporting records may be incomplete. Timing may slip because the claim wasn't ready when the founders thought it was.

That's why I dislike these products for early-stage teams. Founders often hear “secured against the refund” and assume the asset is basically fixed. It isn't. Until a claim is properly assembled and lodged, there's still execution risk.

A quick explainer can help if your finance team wants a visual walkthrough:

Hidden incentives make bad advice more likely

The most important warning isn't just about cost. It's about conflicted recommendations. The Tax Practitioners Board found in its 2025 review that many practitioners failed to provide the required full written disclosure of financial incentives for recommending tax time loans, leaving borrowers unaware of potential bias, according to the TPB review on tax time loans.

That should make every founder stop.

If the person recommending the loan gets paid for the referral and doesn't clearly disclose it, you're not getting clean advice. You're being sold debt inside a trust-based advisory relationship.

Founder test: Ask one direct question in writing. “Do you receive any financial incentive, commission, referral fee, or other benefit if we take this loan?”

Where startups usually get caught

The risk isn't abstract. It tends to show up in a few predictable places:

- Estimated refund risk: Your budget model uses a claim figure that hasn't been pressure-tested against eligible activities and actual evidence.

- Timing risk: The claim prep drifts, AusIndustry registration timing gets compressed, or financial schedules need rework.

- Term risk: Founders focus on “cash this week” and ignore lender controls, repayment mechanics, or personal pressure if the business misses plan.

- Adviser risk: The tax or R&D adviser recommending the product may not be neutral.

If your team is reviewing cash conversion options across finance operations more broadly, this resource for finance operations is useful context because it forces the right question. What asset are you really financing, and how dependable is it?

A lot of founders would benefit more from tightening their claim process than from adding another liability. The ClaimKit blog has practical material on documentation and R&D workflows, but the broader point applies regardless of provider. Better evidence and earlier preparation reduce financing pressure. Loans don't.

Are There Better Alternatives to Tax Rebate Loans?

Usually, yes.

A tax rebate loan is only one way to bridge a timing gap, and for many startups it's not the best one. You should compare it against non-dilutive and dilutive options based on one question: what hurts your company less over the next twelve months?

A simple comparison founders can actually use

| Option | Good fit when | Main drawback |

|---|---|---|

| R&D tax rebate loan | Claim is well-advanced and the gap is genuinely short-term | Cost and claim-dependency |

| Traditional bank facility | Company has enough trading history and clean financials | Harder approval for early-stage startups |

| Investor bridge or SAFE top-up | Existing investors back the business and speed matters | Dilution or future cap table complexity |

| Invoice finance | You have reliable receivables from customers | Useless if the problem is pre-revenue R&D spend |

| Claim acceleration | Documentation exists but process is slow | Requires internal coordination, not just money |

Which option I'd rank first

For pre-seed to Series A tech companies, I'd usually rank the options like this:

- Accelerate the claim process if the business is already eligible and the bottleneck is preparation.

- Use an existing investor bridge if investors already know the company and can move quickly.

- Take a general working capital facility if the business qualifies and terms are clean.

- Use a tax rebate loan only when the claim is strong, timing is tight, and you've exhausted cleaner options.

That order won't apply to every company, but it's a solid default. Early-stage teams shouldn't casually add debt tied to an estimated receivable.

The real decision is about flexibility

Equity is expensive, but so is fragile debt. A bank facility can be sensible if you qualify. Investor capital can be painful but straightforward. Tax rebate loans sit in an awkward middle ground. They often look non-dilutive, but they narrow your room to manoeuvre at exactly the point your forecast is already under strain.

If one month of delay in your refund creates a major problem, the loan hasn't removed risk. It has concentrated it.

That's why I prefer decisions that improve optionality. If an option buys time without creating a brittle repayment scenario, it's usually the better founder choice.

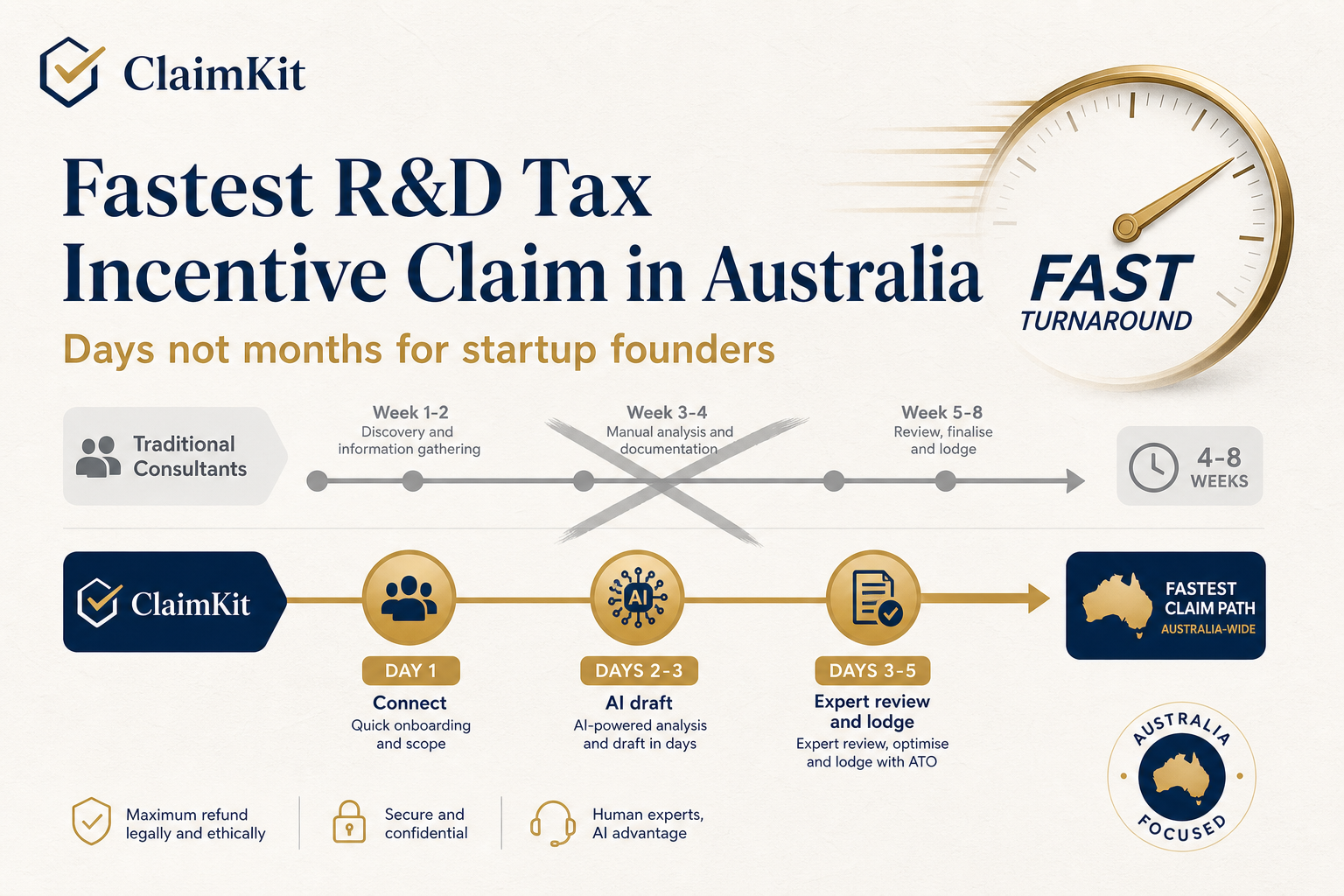

Can You Avoid a Loan by Accelerating Your R&D Claim?

Yes, often you can. Not by cutting corners, but by doing the work earlier and using better source evidence.

The strongest alternative to a tax rebate loan is simple: get the claim into shape sooner, with less manual chasing, fewer document gaps, and cleaner narratives tied to the work your team did.

Why acceleration works better than borrowing

Borrowing solves timing by adding a liability. Claim acceleration solves timing by improving execution. That's a better trade.

Eligible R&D activities must aim to generate new knowledge, follow a systematic progression involving hypothesis and experimentation, and have uncertain outcomes. That's exactly why contemporaneous records from tools like Jira and GitHub matter for fast, compliant preparation, as noted in High Growth Ventures' guidance on navigating R&D tax incentives for startups.

For software companies, the winning move is usually operational, not financial. Pull evidence from the systems your team already uses. Link technical uncertainty to commits, tickets, specs, experiments, retros, and cost records. Then review it properly before lodgement.

What good claim acceleration looks like

A practical workflow looks like this:

- Engineering evidence first: Pull from GitHub, Jira, Linear, or Notion so the technical story starts with what occurred.

- Finance reconciliation second: Tie eligible spend back to Xero or your finance stack before anyone starts making broad assumptions.

- Narrative drafting after the evidence: Don't write the claim from memory months later if the tools already hold the timeline.

- Expert review before lodgement: Automation is useful. Unreviewed automation is not enough.

Modern tooling changes the economics. Platforms like ClaimKit connect systems such as GitHub, Jira, Linear, Notion, and Xero, generate draft narratives and schedules, and pair that with expert review and ATO lodgement support. That model is different from the old black-box advisory approach where founders spend weeks exporting files, answering repetitive questionnaires, and waiting for a PDF draft.

What to do this week

If you want to reduce the odds that you'll need a loan at all, do these four things now:

- Map projects to uncertainty. Identify which engineering work involved technical unknowns.

- Export source records. Pull tickets, commits, specs, meeting notes, and cost data while the trail is still fresh.

- Set an internal EOFY deadline. Don't wait until after year-end to decide what you're claiming.

- Choose a preparation model. Manual adviser, boutique consultant, or software-assisted workflow with expert review. Pick one and start.

Faster claims come from better evidence pipelines, not from writing more persuasive prose at the end.

A Founder's Checklist for Choosing a Funding Path

If you need a practical decision list, use this one. It's blunt because it needs to be.

Start with the cash problem, not the product

- Define the gap: Is this a two-week timing issue, a quarter-long burn issue, or a broken budget?

- Separate urgency from importance: Payroll urgency can push founders into bad debt decisions. Don't let panic choose your funding path.

- Model the downside: Assume the claim takes longer or lands lower than expected. If the loan still works, keep considering it. If it doesn't, walk away.

Compare advisers by operating model

Founders often compare providers by fee headline alone. That's a mistake. Compare them by speed, transparency, and how they gather evidence.

| Provider type | Examples | What to look for |

|---|---|---|

| Traditional advisory firms | Treadstone, Prime Partners | Deep process, but ask about turnaround time and who does the drafting |

| Boutique specialists | Link R&D Advisory, Bulletpoint | Closer service, but check documentation workflow and review depth |

| Software-led workflow with expert review | Modern platforms | Better integrations, visibility, and speed if the process is well designed |

No need for tribalism here. Different models suit different companies. A complex claim may suit a traditional or boutique adviser. A software-heavy startup with strong systems may benefit from an integration-led workflow. What matters is whether the provider helps you prepare an audit-ready claim without turning the process into a scramble.

The short list you should actually ask

Before you commit to a lender or adviser, ask:

- How is the claim evidenced?

- Who reviews the technical narrative?

- What happens if expected claim value changes?

- Are any loan referrals incentivised?

- Can the provider show a transparent process from evidence gathering to lodgement?

If you want to compare advisor models and workflows, the ClaimKit consultants page is one reference point for how software-assisted and expert-reviewed support can be structured.

Frequently Asked Questions About R&D Funding

Can temporary visa holders get tax rebate loans tied to an R&D refund

Sometimes, but the structure is messy. A common issue is that many tax rebate loan products are built around specific temporary visa categories and may exclude permanent residents, while the R&D Tax Incentive itself requires Australian corporate residency. That creates a genuine mismatch for non-permanent resident founders using an Australian company structure, as outlined in Cash Direct's visa tax advance information.

The practical answer is this. Don't assume founder visa status and company eligibility line up neatly with a lender's product rules. Check the company's tax residency and the lender's borrower criteria separately.

When should we start preparing our R&D claim around EOFY

Earlier than you think. The best time is while the work is happening and the records are still easy to gather. If you wait until after EOFY to reconstruct experiments, decisions, and development history, preparation gets slower and weaker.

For software teams, that usually means reviewing GitHub, Jira, Linear, Notion, and finance records before year-end close, not after.

How do I tell if an R&D adviser is actually helping or just adding process

Look at the evidence flow. A good adviser or platform should be able to explain how they identify eligible activities, gather contemporaneous records, draft the technical narrative, review financial schedules, and support lodgement. If the process feels opaque, it probably is.

Also ask whether any loan recommendation comes with a financial incentive. If the answer isn't clear and written down, treat that as a warning sign.

Should I use a loan if my refund is already expected

Only if the claim is already well-supported, your timing gap is real, and you've compared cleaner options first. “Expected” doesn't mean “received”. A startup should only borrow against a future tax outcome when the operational risk is already under control.

For more operational questions about process, handling data, and platform use, the ClaimKit privacy and support resources are a useful place to start.

If you want a faster, more transparent way to prepare an R&D claim without defaulting to debt, take a look at ClaimKit. It combines AI-drafted claims, expert review, ATO lodgement support, and integrations with GitHub, Jira, Linear, Notion, and Xero so founders and finance teams can tighten documentation and move earlier with more confidence.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.