Australian tax agent requirements are straightforward in principle and strict in practice. A registered tax agent typically needs relevant tertiary study, specific Australian tax law coursework, recent supervised experience, to satisfy the TPB's fit and proper person test, and to maintain professional indemnity insurance before providing tax agent services for a fee.

If you're a founder about to engage an R&D advisor, this matters more than most firms admit. The issue isn't just whether someone “knows R&D”. It's whether they can legally prepare, review, lodge, and stand behind work that affects your company's tax position when the ATO asks questions later.

For software startups, the risk is sharper again. Your claim usually sits across GitHub commits, Jira tickets, product specs in Notion, payroll records, contractor invoices, and finance data in Xero. If your advisor isn't properly registered, or if they can't run a disciplined evidence process, you're taking compliance risk where you should be reducing it.

Table of Contents

- Why Must My Advisor Be a Registered Tax Agent

- What Are the Core Requirements to Become a Tax Agent

- What Are an Agent's Ongoing Professional Obligations

- How Can I Verify My R&D Tax Advisor Is Registered

- How Do Agent Requirements Affect Your R&D Tax Claim

- Frequently Asked Questions About Tax Agents

- Can my accountant or bookkeeper handle my R&D claim?

- Can an unregistered advisor help draft the claim if a registered agent lodges it?

- What's the consequence if I use an unregistered provider without realising it?

- How do I compare a traditional firm with a platform-based provider?

- What should I ask in the first call with an R&D advisor?

Why Must My Advisor Be a Registered Tax Agent

You don't need an abstract legal lecture here. You need to know whether the person charging to help with your R&D claim can lawfully do the work.

In Australia, the Tax Practitioners Board says anyone charging a fee for a service they know, or should reasonably know, is a tax agent service must be a registered tax agent under section 50-5 of the Tax Agent Services Act 2009. The TPB also makes clear that this covers preparing returns, notices, statements, applications or other documents about a client's taxation-law liabilities, obligations or entitlements, and lodging those documents on a client's behalf, as set out in the TPB guidance on tax agent services.

That's the practical line founders need to understand. Registration isn't about prestige. It's about whether the person is allowed to do fee-charging work that changes or supports your statutory tax position.

What this means for an R&D startup

A lot of founders assume any accountant, CFO-for-hire, bookkeeper, or startup advisor can “sort the claim”. Sometimes they can help with inputs. That doesn't mean they can legally provide the tax agent service itself.

If someone is preparing your R&D schedules, shaping the tax position, and dealing with lodgement or ATO-facing work for a fee, registration stops being optional. It becomes the baseline compliance requirement.

Practical rule: If an advisor is charging to prepare or lodge tax documents that affect your company's tax entitlements, check registration before you sign the engagement.

Why founders should care even if the work looks fine

Bad tax work often looks polished. A clean PDF, a tidy spreadsheet, and confident language don't tell you whether the process behind it is compliant.

Registration matters because it puts the advisor inside a regulated framework. The TPB screens who can enter that framework, and that creates a minimum standard of capability and accountability. If you skip that check, you may still get a claim filed. You just may not like the position you're left defending later.

For a founder, the simplest filter is this: don't hire on sales confidence alone. Hire on legal authority, technical competence, and whether the person can explain their evidence process in plain English. If they can't do that, move on.

If you want to know who's behind a provider and how they describe their role, review the ClaimKit team and company background the same way you'd review any other adviser. Treat that as basic diligence, not brand research.

What Are the Core Requirements to Become a Tax Agent

You hire an R&D advisor, give them access to Jira tickets, GitHub commits, and Xero exports, and assume the hard part is proving the technical story. It isn't. The first control point is simpler. Is the person giving tax advice qualified and authorised to do it?

That question matters because tax agent registration is not just a credential. It is the entry standard for anyone who wants to prepare tax positions for a fee. For founders, it is a practical screening tool. It tells you whether your advisor has met baseline education, experience, conduct, and insurance requirements before they touch a claim that could later be reviewed.

Education and recent experience

A tax agent does not qualify by sounding commercial or knowing startup jargon. The pathway usually requires formal study, approved tax law education, and recent relevant experience. The Tax Institute summary of tax agent qualification pathways explains that applicants may need an accountancy degree, Board-approved Australian tax law courses, and recent work experience before registration.

For R&D claims, that matters more than founders often realise. Software claims involve judgement about eligible activities, apportionment, evidence quality, and how development records support the tax position. An advisor who cannot connect tax rules to your actual systems is not ready to lead the work.

Ask how they use your source records. A credible advisor should be able to explain how they review sprint history in Jira, code activity in GitHub, and financial records in Xero to support the claim. If the process relies on founder interviews and a spreadsheet built at year end, your risk goes up fast.

Character and insurance

Registration also depends on personal suitability and insurance cover. Applicants must be adults, satisfy qualification and experience pathways, meet the fit and proper person test, and hold professional indemnity insurance that meets TPB standards.

Founders should care about both.

The fit and proper person test is the conduct filter. It exists because tax agents are trusted to form and defend tax positions, not just complete paperwork. Professional indemnity insurance is the financial backstop. If advice is careless and the claim causes loss, there needs to be a real framework around responsibility.

Do not treat either point as admin.

The firm must be structured properly too

A common founder mistake is checking the company brand and stopping there. If a firm or platform provides tax agent services, registered individual tax agents still need to sit inside the delivery model with enough control and supervision over the work.

That is where modern R&D workflows need scrutiny. Plenty of providers use analysts, questionnaires, AI-assisted drafting, and document collection portals. That can be efficient. It only works safely if a registered agent is reviewing the evidence, making the judgement calls, and taking responsibility for the tax work. The process should stay compliant whether you use a traditional advisory firm or a software-enabled workflow such as ClaimKit's R&D tax claim platform.

Use this checklist before you engage anyone:

| What to ask | Why it matters |

|---|---|

| Who is the registered individual responsible for my claim? | The legal responsibility sits with a person, not a brand |

| What tax training and recent experience do they have? | R&D claims depend on current judgement, not generic tax knowledge |

| How do they review Jira, GitHub, and Xero records? | Good claims are built from contemporaneous evidence, not reconstructed stories |

| Who supervises junior staff or automated workflows? | Support staff and software can assist, but registered agents must control the tax advice |

| Is professional indemnity insurance in place? | It shows the practice is operating inside a regulated risk framework |

A founder does not need to memorise the registration rules. You do need to test whether your advisor can show a qualified person, a supervised process, and an evidence method that matches how your company builds product. If they cannot show all three, keep looking.

What Are an Agent's Ongoing Professional Obligations

Registration isn't a one-off badge. It only means something if standards keep being maintained after approval.

That's especially relevant in a profession with an older demographic profile. According to TPB demographic data reported by Accountants Daily, 58% of individual tax agents were over 50 years old as at 30 April 2025, as discussed in this report on the ageing tax practitioner population. In a mature profession, ongoing obligations matter because legislation, ATO focus areas, and R&D compliance expectations don't stand still.

Why continuing education matters in startup tax work

R&D claims don't fail only because someone misunderstood the rules from day one. They also fail because an advisor kept using old assumptions, stale templates, or weak documentation habits long after the environment changed.

A serious tax agent should be maintaining current technical knowledge. For founders, that shows up in practical ways. They ask better scoping questions. They care about contemporaneous evidence. They don't treat software development as a vague “innovation” narrative disconnected from source records.

An advisor who can't explain current record-keeping expectations in plain language is already giving you a warning sign.

Conduct matters as much as competence

The other side of ongoing obligation is professional conduct. Founders should expect honesty about grey areas, sensible limits on what can be claimed, and transparent communication about evidence gaps.

That matters when you're under EOFY pressure. A weak advisor will tell you what you want to hear. A good one will tell you what can be defended.

Use a simple standard when screening firms:

- Ask direct questions: Who reviews the final claim, and what documentation do they insist on?

- Watch for overclaim language: If someone talks like every engineering activity is automatically eligible, be cautious.

- Check the paperwork: Read the provider's terms and engagement wording, including documents like ClaimKit's terms, to see how responsibility, scope, and review are described.

How Can I Verify My R&D Tax Advisor Is Registered

Your founder signs an engagement letter on Friday. Three months later, the R&D claim is drafted, the fees are accruing, and you still cannot tell who the registered tax agent is. That is a procurement failure you can avoid in one short call.

Verification should be fast and slightly uncomfortable for the provider if their setup is weak. Ask for the exact name of the individual tax agent responsible for your claim. If you are hiring a firm, ask who supervises the work, who reviews the final position, and which entity is contracted to provide the tax agent services.

Five checks I would do before sharing a single export from Jira or Xero

-

Get the exact legal name

Ignore the brand name on the website if necessary. You need the legal name of the person and, if relevant, the entity engaged to provide the service. -

Identify the registered person who is accountable

Ask a direct question. Who is the registered tax agent responsible for my R&D claim? If the answer is vague, keep pushing. -

Check the firm structure, not just the salesperson

A polished R&D sales process tells you nothing about registration. You need to know whether the firm has the right supervision arrangement behind the scenes. -

Confirm the registration is current

“Experienced,” “specialist,” and “ex-Big Four” are marketing labels. Current registration is what matters here. -

Test how the registration connects to the workflow

Ask who reviews the technical narrative, who checks eligibility calls, and who signs off before lodgement. For software startups, ask how they use records from GitHub, Jira, Linear, Notion, payroll, and Xero in that review process.

That last point matters more than founders expect. A registered name on paper is not enough if the actual work is being pushed through a junior team with weak supervision and no clean link between engineering records and the tax position.

Red flags that should stop the buying process

Some providers make this easy. Good. That is what you want.

Others do one of the following:

- They dodge the accountability question: nobody will name the registered person.

- They hide behind the firm brand: you hear about the company, never the individual responsible.

- They split sales from compliance: the closer promises outcomes, but cannot explain review or sign-off.

- They treat your records like an afterthought: no clear method for tying Jira tickets, GitHub commits, or finance data to the claim.

- They make verification feel awkward: that usually means the operating model falls apart under scrutiny.

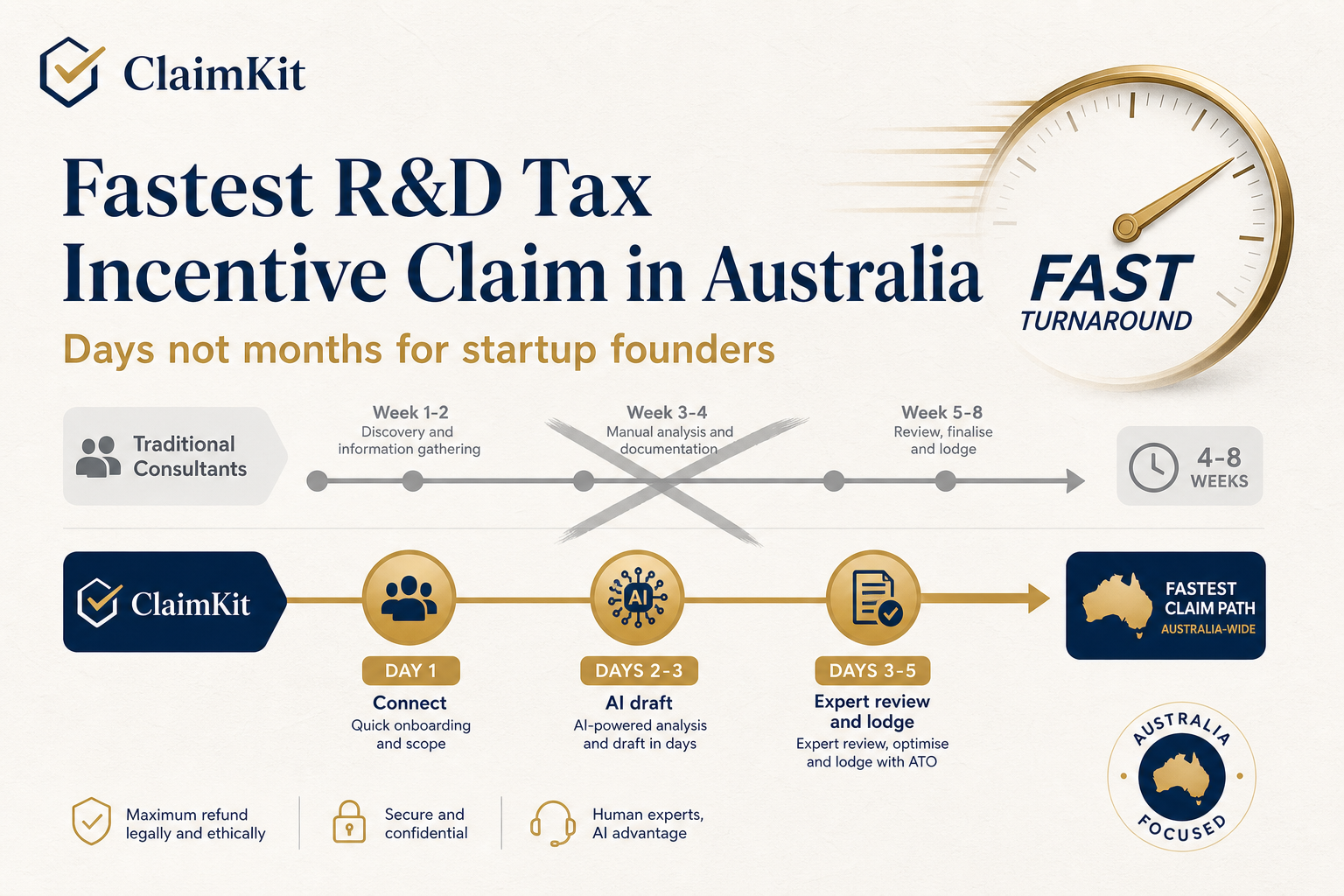

This walkthrough gives a visual overview of the checking mindset founders should bring to advisor selection:

You should also compare how providers describe their adviser model in public. If a platform explains who its advisers are, how review works, or how claims are handled, read that before you sign. One useful example is ClaimKit's consultant network and service model.

If you cannot identify the registered tax agent, the supervising process, and the evidence workflow before kickoff, do not hand over your R&D claim. Your company carries the risk, not the sales team.

How Do Agent Requirements Affect Your R&D Tax Claim

For R&D work, registration is necessary but nowhere near sufficient. A registered agent can still run a weak process. That's the point too many founders miss.

The standard is shifting from basic credentialing toward process maturity. As compliance scrutiny on contemporaneous records tightens, the strongest advisers don't just know the law. They can trace every narrative claim back to source material in your operating systems.

What process maturity looks like in a software startup

For a tech company, evidence is scattered by default. Engineering history sits in GitHub, Jira, or Linear. Product context may sit in Notion. Cost records often sit in Xero and payroll systems.

A credible R&D advisor should be able to answer questions like these without hand-waving:

- How do you connect technical narratives to source records?

- How do you track who reviewed the claim and when?

- How do you handle gaps between engineering activity and finance records?

- How do you document judgement calls on eligibility and apportionment?

The underlying issue is captured well in the observation that the requirement for R&D claims is shifting from mere credentialing to process maturity, with stronger need for workflow controls and source-data traceability in software development contexts, as discussed in this analysis of modern tax-agent process expectations.

Traditional advisory versus platform-based workflows

Provider models start to differ in a way founders should care about. Traditional firms such as Treadstone, Prime Partners, Link R&D Advisory, and Bulletpoint may rely more heavily on interviews, documents sent over email, and manual drafting. That model can work, but only if the firm is disciplined about version control, evidence capture, and registered review.

Platform-based models push in a different direction. ClaimKit, for example, is a blogging and product platform for R&D claim workflows that says it drafts claim materials from tools such as GitHub, Jira, Linear, Notion, and Xero, with expert review and ATO lodgement in the process. For a founder, the useful question isn't whether software is involved. It's whether the workflow improves traceability and keeps a registered professional accountable for the final position.

Don't choose between “human” and “software”. Choose the process that gives you better records, clearer review, and less room for unsupported claims.

What you should do this week

If you're hiring now, take these actions immediately:

- Map your evidence stack: List where technical work, product decisions, and costs reside.

- Ask every advisor for their review workflow: Not a brochure. The specific review chain.

- Test for traceability: Ask how a sentence in the technical narrative gets tied back to a ticket, commit, spec, or invoice.

- Pressure-test EOFY readiness: If your records are messy, fix the collection process before the claim drafting starts.

- Use the government overview as a baseline: Read the business.gov.au R&D Tax Incentive guidance so you can separate scheme basics from adviser marketing.

Frequently Asked Questions About Tax Agents

Can my accountant or bookkeeper handle my R&D claim?

Maybe parts of the workflow, but don't assume they can do the tax agent service itself. An accountant or bookkeeper may help organise records, reconcile costs, or prepare supporting schedules. If they're charging for work that is a tax agent service, registration becomes the key issue.

Can an unregistered advisor help draft the claim if a registered agent lodges it?

Founders can run into trouble. Support work can exist around a claim, but you shouldn't treat “a registered person lodges it later” as a cure-all. Ask who is ultimately responsible for review, judgement, and supervision throughout the engagement. If that answer is fuzzy, the setup is risky.

What's the consequence if I use an unregistered provider without realising it?

The immediate problem is loss of confidence in the process behind the claim. You may end up with weak records, poor legal framing, or unsupported positions that become expensive to clean up later. Even if the claim is lodged, you've increased your operational risk for no good reason.

How do I compare a traditional firm with a platform-based provider?

Use the same checklist for both. Who is the registered tax agent? How is evidence collected? What gets reviewed manually? How do they handle GitHub, Jira, Linear, Notion, and Xero data? How is lodgement controlled? The delivery model matters less than the discipline behind it.

What should I ask in the first call with an R&D advisor?

Ask five things. Who is the registered agent responsible for my claim? How do you assess eligibility? What records do you need from engineering and finance? How do you document review decisions? What happens if evidence is incomplete? If they can't answer cleanly, keep looking.

If you want a more structured way to prepare an R&D claim, ClaimKit is one option to review. It's built around AI-drafted claim materials from tools like GitHub, Jira, Linear, Notion, and Xero, with expert review and lodgement support, which is useful if you want tighter evidence handling rather than another email-heavy process.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.