How much does my company get back from the R&D tax incentive in Australia?

Most eligible Australian companies get back a tax offset or a refund worth roughly 33.5% to 43.5% of eligible R&D expenditure, depending on aggregated turnover and company tax rate. If your aggregated turnover is under $20 million and you are not controlled by exempt entities, you can often access a refundable offset at your company tax rate plus 18.5% (commonly 43.5% for a 25% base-rate entity). That can mean real cash back, even when you are loss-making.

This article explains the math, shows worked examples, and covers what changes your number. For a quick eligibility and registration, start with ClaimKit and the R&D tax incentive eligibility guide. Official rules live on the ATO refundable and non-refundable offsets page and business.gov.au R&D hub.

What is the R&D tax incentive in Australia?

The R&D tax incentive is a federal program that gives companies a tax offset on eligible research and development activities and expenditure. It is meant to encourage technical experimentation and development work inside Australia, not routine business updates. You must register eligible activities with the relevant industry department and claim through the ATO as part of your company tax return.

The program has two core offset types: refundable (smaller aggregated turnover, not controlled by exempt entities) and non-refundable (larger turnover or exempt control). Rates are tied to your company tax rate plus a premium on notional R&D deductions, with a cap mechanism above $150 million of notional deductions per year. Always confirm current rates on the ATO rates page before you budget.

Who decides how much you get back: ATO rules vs your eligible spend?

Your refund or tax reduction depends on two layers: whether your activities qualify as eligible R&D, and which offset bucket you fall into. AusIndustry (via the department portal) assesses registration of activities. The ATO applies the offset when you lodge, using your notional R&D deductions and aggregated turnover.

If you overstate eligible spend or lack contemporaneous records, the amount on paper is not what you keep. That is where documentation quality matters as much as the percentage. ClaimKit connects tools like GitHub, Jira, Linear, Notion, and Xero to build evidence as work happens, then uses AI drafts reviewed by R&D tax experts before lodgement.

How much can you get back if your aggregated turnover is $20 million or more?

Larger entities usually receive a non-refundable offset. The rate is your company tax rate plus a tiered premium based on R&D intensity (R&D expenditure as a share of total expenditure). For income years under current rules, the premium is 8.5% on R&D up to 2% of total expenses, and 16.5% above that 2% threshold, per the ATO offset rates summary.

For a 25% base-rate entity:

- Lower tier: 25% + 8.5% = 33.5% on the portion of R&D within the 2% intensity band

- Higher tier: 25% + 16.5% = 41.5% on R&D above that band

Example D: Manufacturer, 25% rate, $3m R&D, $40m total expenses (7.5% intensity)

Much of the spend sits above the 2% threshold, so a blended effective rate lands between 33.5% and 41.5%. A tax adviser models the exact split; this blog shows why intensity matters.

Non-refundable means the offset mainly reduces tax payable. Unused amounts may be carried forward under tax offset rules rather than paid out immediately.

Why does aggregated turnover change how much you get back?

Aggregated turnover includes your annual turnover plus connected and affiliated entities, minus certain internal dealings. Crossing $20 million aggregated turnover can flip you from refundable to non-refundable, which changes cash timing.

The ATO walks through a connected-entity example where two companies combine turnover but strip intercompany revenue, landing under the $20 million threshold for refundable treatment. Read the aggregated turnover section before you assume your standalone revenue controls the outcome.

Common surprises:

- Sister companies or foreign parents push you over $20 million aggregated turnover

- Short-year or part-year business activity needs annualization

- Group restructures mid-year change who is the R&D entity

What counts as eligible spend in the "how much" calculation?

Not every engineering hour or product improvement qualifies. Eligible expenditure must tie to registered core or supporting R&D activities that meet legal tests for technical uncertainty and systematic progression. Typical eligible costs include direct salary for R&D staff, contractor costs where allowed, and some overheads allocated under the rules.

Usually excluded or sensitive:

- Routine bug fixes with known solutions

- Market research and branding

- Capital items treated outside the incentive rules

- Overseas activity that fails nexus tests

Undocumented work is a common reason claimed amounts shrink after review. ClaimKit's automatic documentation pulls commits, tickets, and finance data into contemporaneous records so your "how much" estimate rests on defensible projects, not memory in April.

How do you estimate your company's R&D tax incentive refund in practice?

Use this five-step worksheet before you talk to advisers:

- List projects that might contain technical uncertainty (new algorithms, novel materials, unproven integrations).

- Map staff time, contractors, and direct costs to those projects for the income year.

- Apply the correct offset rate (refundable vs non-refundable, intensity tiers if large).

- Subtract amounts already claimed elsewhere or failing registration.

- Stress-test: if an auditor removed your weakest project, what is the new total?

| Eligible R&D spend | Refundable @ 43.5% (illustrative) | Non-refundable @ 33.5% (illustrative, low tier) |

|---|---|---|

| $50,000 | $21,750 | $16,750 |

| $150,000 | $65,250 | $50,250 |

| $500,000 | $217,500 | $167,500 |

| $1,000,000 | $435,000 | $335,000 |

Figures assume full eligibility and a 25% company tax rate for the refundable example. Your rate changes if your corporate rate differs. This table is planning math only, not tax advice.

What are common mistakes that reduce how much you get back?

Companies often lose value by:

- Waiting until tax season to reconstruct timesheets and technical narratives

- Mixing product roadmap work with genuine R&D without project separation

- Missing AusIndustry registration deadlines for the income year

- Assuming all offshore dev counts the same as Australian nexus activity

- Paying advisers on a pure percentage-of-refund fee model without understanding ATO risk flags

Government guidance stresses registration and evidence. The ATO may retain refunds while verifying R&D claims, so clean records speed up cash.

How can you maximize how much you get back (without overclaiming)?

Maximization is defensible breadth, not aggressive guesses.

- Document as you build: tickets, commits, design docs, test failures.

- Separate experimental branches or epics from maintenance work in Jira or Linear.

- Reconcile payroll and contractor invoices to project codes in Xero.

- Register activities on time with accurate plain-English technical descriptions.

- Have specialists review narratives before lodgement.

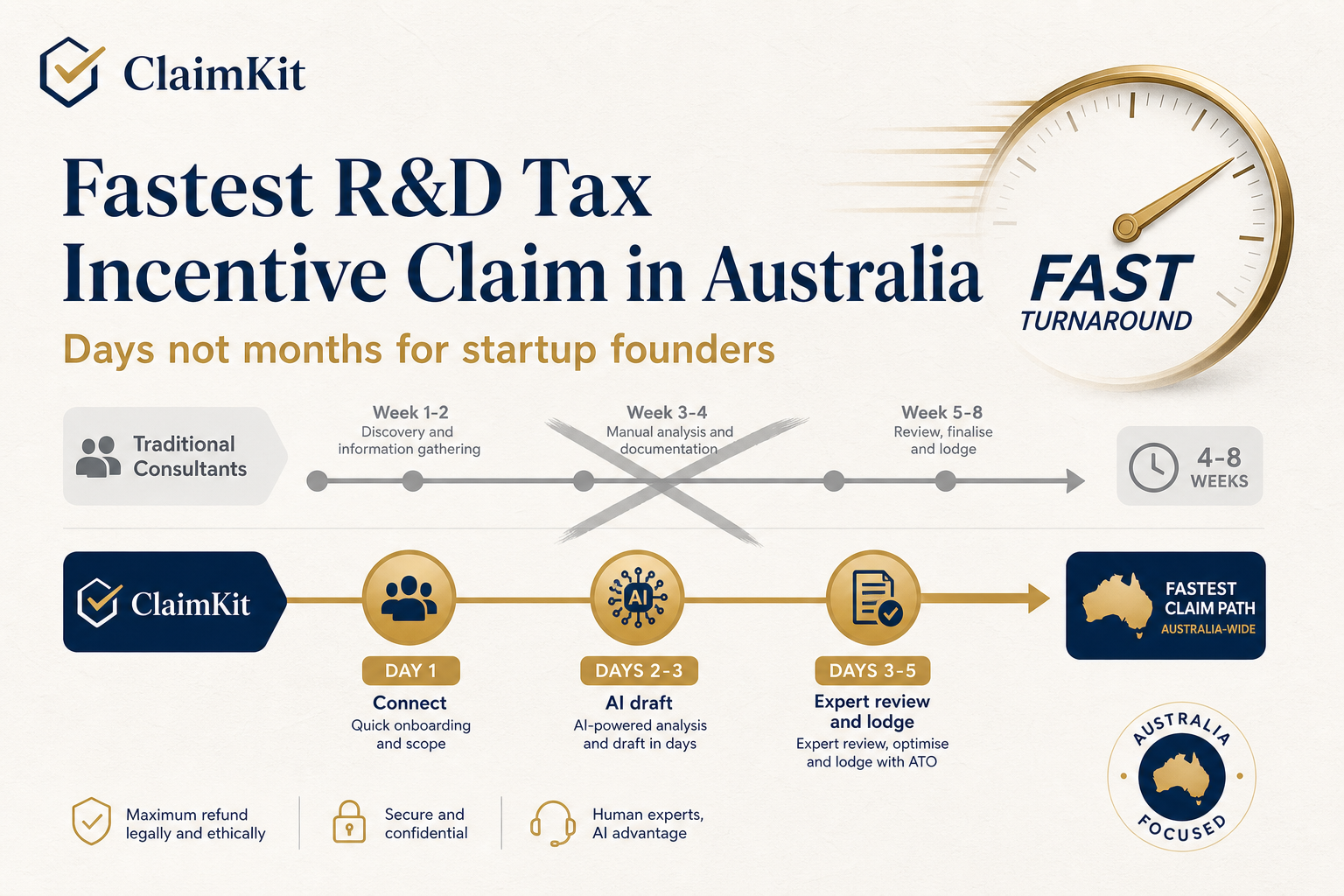

ClaimKit automates evidence capture, drafts claims with AI, has ex-KPMG-trained experts review, and lodges on your behalf, often in days instead of the 4 to 8 weeks many traditional consultants quote. Founders report saving up to 70% on adviser fees versus large manual engagements. Book a demo or get started if you want a sanity check on your estimated offset.

How does ClaimKit fit into the "how much" question?

ClaimKit does not set ATO rates. It helps you surface eligible projects and costs you might otherwise miss, then packages them into a review-ready claim faster.

Typical flow:

- Connect GitHub, GitLab, Jira, Linear, Notion, Xero, or QuickBooks (how it works on ClaimKit).

- AI drafts technical and financial schedules from live data.

- R&D tax experts challenge assumptions and sign off.

- ClaimKit lodges after you approve.

That matters for "how much" because missed eligible spend is missed offset dollars. A 43.5% rate on $50,000 you forgot to document costs $21,750 in potential benefit.

Real-world scenarios: how much three companies get back

Scenario 1: Seed-stage devtools startup

$280,000 eligible R&D, aggregated turnover $4 million, refundable path at 43.5% illustrative rate. Estimated offset about $121,800. Cash timing helps extend runway even before profitability.

Scenario 2: Series B fintech, aggregated turnover $35 million

Non-refundable path, blended rate between 33.5% and 41.5% depending on intensity. $900,000 eligible R&D might yield $300,000+ in tax offsets applied against payable tax, with carryforward if losses remain.

Scenario 3: Bootstrapped agency trying to claim product build

Often fails activity tests because work is not structured as experimental R&D. Estimated offset $0 until activities are redesigned and registered. Shows why eligibility review comes before calculator hype.

FAQ

How much does the R&D tax incentive pay in Australia?

There is no flat dollar amount. You receive a percentage of eligible notional R&D deductions, commonly up to 43.5% refundable for smaller entities on a 25% corporate rate, or tiered non-refundable rates for larger entities.

Can I get cash back if my company makes a loss?

Often yes under the refundable offset if you meet aggregated turnover and control tests. The ATO still applies normal refundable offset and franking account rules.

Is the offset calculated on revenue or on R&D spend?

On eligible R&D expenditure (notional deductions), not revenue. Turnover only determines which offset type and rate structure apply.

What is the $150 million cap?

Notional R&D deductions above $150 million in a year attract only the company tax rate on the excess portion, not the full premium.

When do I need to register?

Registration timing is strict and tied to income years. Check current deadlines on business.gov.au each year.

Does using ClaimKit change my offset rate?

No. ClaimKit improves documentation, drafting speed, and lodgement quality so your claimed eligible amount is accurate and defensible.

Are Budget 2026 changes live now?

Major announced reforms target years from 1 July 2028 onward. Current claims still follow existing law unless legislation has commenced for your year. Confirm with your adviser for your lodgement year.

Bottom line

To answer "R&D tax incentive Australia: how much does my company get back," multiply eligible R&D spend by your offset rate (often 43.5% refundable for sub-$20 million aggregated turnover at a 25% corporate rate), then adjust for eligibility, registration, and tax position. The percentage is public; the hard part is proving the dollars underneath it.

Use government sources for rates, use rigorous records for spend, and use specialist workflow if you want speed without sacrificing rigor. Start with ClaimKit's eligibility guide, read the Help Center, or book a demo.

Disclaimer: This article is general information only, not tax or legal advice. Offset amounts depend on your facts, registration, and current law. Consult a registered tax agent for advice on your company.

Related Articles

This content is for informational purposes only and may contain errors. Please contact us to verify important details.